yahoo Press

Why Investors Own VOOG for Growth Not Its Tiny 0.46% Dividend

Images

1 / 5

2 / 5

3 / 5

4 / 5

5 / 5

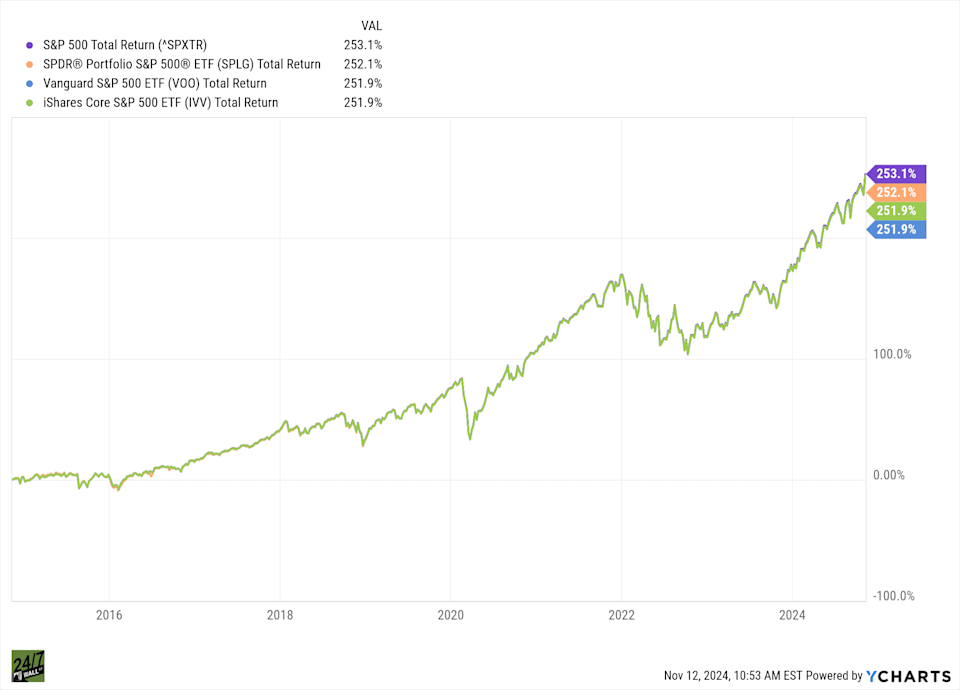

Vanguard S&P 500 Growth Index Fund ETF Shares (NYSEARCA:VOOG) offers a yield of just 0.46%, a byproduct of owning growth companies rather than a reason to own the fund, and investors evaluating that income need to understand what drives it before deciding if it fits their strategy. VOOG tracks the S&P 500 Growth Index, a subset of the S&P 500 that screens for companies with strong revenue growth, earnings growth, and price momentum. The result is a portfolio dominated by mega-cap technology and communication services names, with Information Technology representing 41.4% of the fund and a single holding, Nvidia, accounting for nearly 14% of the entire portfolio. These are businesses that reinvest aggressively rather than pay out cash, which explains why the fund's dividend yield sits at just 0.46%. For context, the 10-year Treasury yield is near 4.35%. An investor holding VOOG for income is accepting a yield roughly one-tenth of what a risk-free government bond pays. The income here is simply a byproduct of owning growth companies. The chart displays the total return performance of S&P 500, SPDR, Vanguard (VOO), and iShares (IVV) ETFs from approximately 2015 to 2024. VOOG passes through dividends collected from its underlying holdings. Most of the fund's weight sits in companies that pay little or nothing: Nvidia, Alphabet, Meta, Amazon, and Tesla collectively represent a large share of assets, and none are known for generous payouts. The income that does flow through comes primarily from more mature holdings like Apple, Microsoft, Visa, and JPMorgan Chase, which appear in the top 12 positions. The fund pays quarterly. In 2025, the four quarterly distributions totaled $2.18 per share, compared to $1.79 per share across all four payments in 2024. That looks like growth, but the comparison is misleading: 2023 distributions totaled $3.05 per share, well above either subsequent year. The variability reflects how dividend pass-through ETFs work: the fund distributes whatever dividends its holdings pay, and that can shift meaningfully as the portfolio's composition and individual company payouts change. Read: Data Shows One Habit Doubles American’s Savings And Boosts Retirement Most Americans drastically underestimate how much they need to retire and overestimate how prepared they are. But data shows that people with one habit have more than double the savings of those who don’t. The swings in VOOG's quarterly distributions, ranging from about $0.30 in Q1 2024 to nearly $0.91 in Q4 2023, reflect portfolio rebalancing, changes in the index's composition, and the timing of special dividends from underlying holdings rather than financial distress. The fund itself has no payout ratio to analyze because it simply passes through what it collects. The expense ratio is 0.08%, essentially negligible, meaning almost nothing is lost between what the holdings pay and what investors receive. The fund holds $21.9 billion in net assets, providing ample liquidity and operational stability. VOOG is down 8.2% year-to-date through March 31, compared to a 4.4% decline for VOO over the same period. The growth tilt amplifies both upside and downside: VOOG returned 22.5% over the past year versus 17.7% for VOO, but the current drawdown is also steeper. The VIX is near 25, placing market volatility in the elevated uncertainty range. Rising Treasury yields and macro uncertainty around tariffs have pressured growth stocks disproportionately. A fund yielding 0.46% that has lost 8% of its value this year has produced a negative total return for 2026 so far, regardless of how reliably the quarterly checks arrive. VOOG's distributions carry no commitment to a specific payout level. They will fluctuate with whatever its growth-oriented holdings pay, and those payments are structurally small. Over a decade, VOOG has returned 330%, which is the actual argument for owning it. Long-term investors drawn to large-cap growth exposure at minimal cost will find the quarterly distributions a small bonus on top of price appreciation. Those who need reliable income to cover expenses will find the yield too small and too variable to depend on. Most Americans drastically underestimate how much they need to retire and overestimate how prepared they are. But data shows that people with one habit have more than double the savings of those who don’t. And no, it’s got nothing to do with increasing your income, savings, clipping coupons, or even cutting back on your lifestyle. It’s much more straightforward (and powerful) than any of that. Frankly, it’s shocking more people don’t adopt the habit given how easy it is.