yahoo Press

Allegion's Q1 2026 Earnings: What to Expect

Images

1 / 5

2 / 5

3 / 5

4 / 5

5 / 5

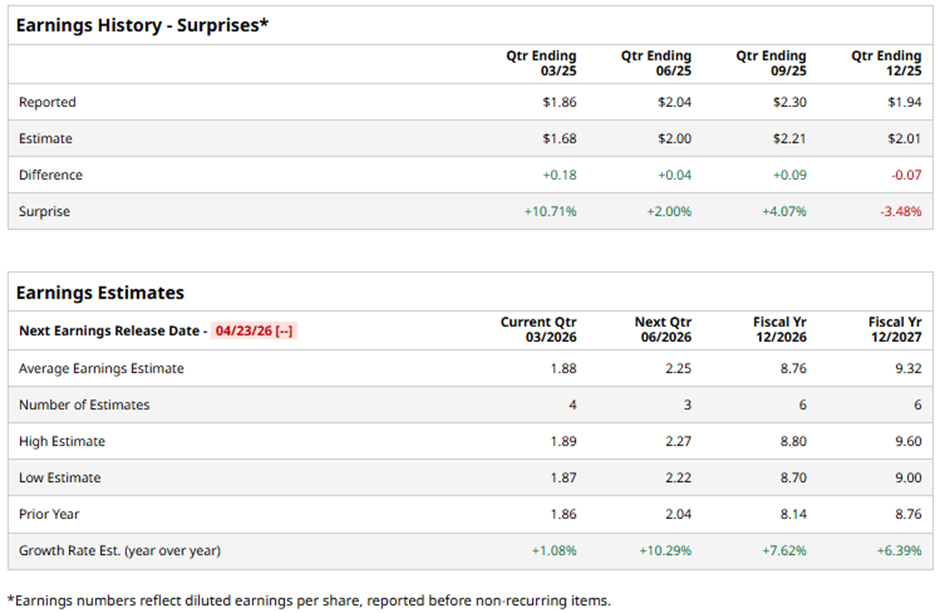

With a market cap of $12.3 billion, Allegion plc (ALLE) is a global provider of security products and solutions, operating through its Allegion Americas and Allegion International segments. The company offers a wide range of door hardware, electronic access control systems, and security software, serving commercial, institutional, and residential markets worldwide. The Dublin, Ireland-based company is expected to release its fiscal Q1 2026 results soon. Ahead of this event, analysts project Allegion to report an adjusted EPS of $1.88, a 1.1% rise from $1.86 in the year-ago quarter. It has exceeded Wall Street's bottom-line estimates in three of the last four quarters while missing on another occasion. Trump Says Micron Is One of the 'Hottest' Stocks. Does That Make MU a Buy Here? Stocks Set to Open Higher as Bond Yields Fall on Fading Rate-Hike Bets, U.S. Jobs Data and Powell’s Remarks Awaited Micron Stock Cools Off — Is MU Now Too Cheap to Ignore? Markets move fast. Keep up by reading our FREE midday Barchart Brief newsletter for exclusive charts, analysis, and headlines. For fiscal 2026, analysts forecast the security device maker to report adjusted EPS of $8.76, up 7.6% from $8.14 in fiscal 2025. Over the past 52 weeks, Allegion has increased 11.4%, underperforming the broader S&P 500 Index's ($SPX) 13.7% return and the State Street Industrial Select Sector SPDR ETF's (XLI) 20.3% gain over the same period. Shares of Allegion plunged 9.4% on Feb. 17 as investors reacted to a cautious outlook, especially expectations of continued weakness in U.S. residential markets after high single-digit declines, despite total Q4 2025 revenue growth of 9.3% to $1.03 billion. Although the company guided 2026 adjusted EPS at $8.70-$8.90 and projected total revenue growth of 5%–7%, the outlook pointed to modest organic growth of 2% - 4% and a heavier reliance on pricing over volume. Concerns were further amplified by ongoing volume declines in residential and international segments, softer demand trends, and questions around capital allocation after about $630 million in M&A spending in 2025. Analysts' consensus view on Allegion stock is cautiously optimistic, with a "Moderate Buy" rating overall. Among 12 analysts covering the stock, three suggest a "Strong Buy" and nine give a "Hold." The average analyst price target is $180.50, indicating a potential upside of 26.3% from the current levels. On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. This article was originally published on Barchart.com