yahoo Press

China’s light vehicle market expected to be flat in 2026

Images

1 / 6

2 / 6

3 / 6

4 / 6

5 / 6

6 / 6

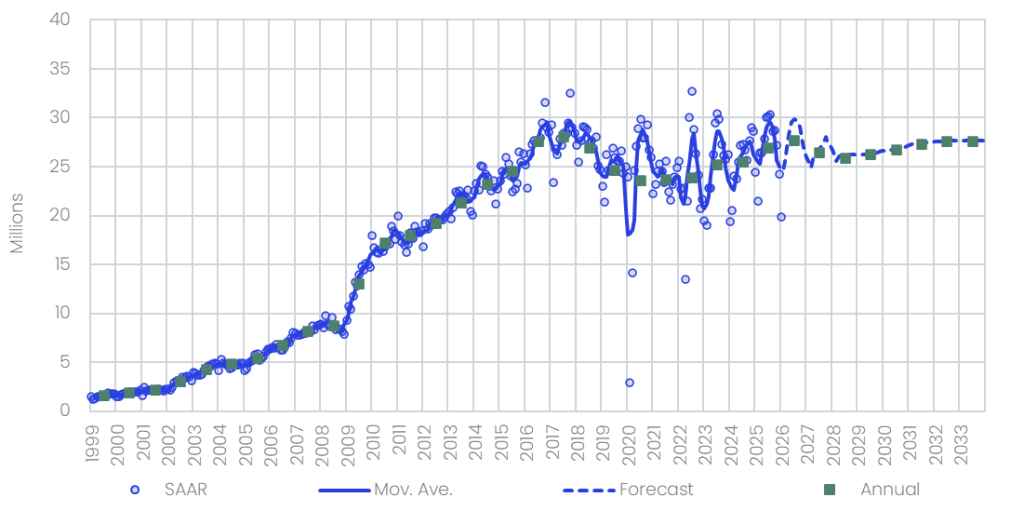

In January 2026, China’s automotive market contracted year-on-year (YoY) amid seasonal disturbances and a high comparison base. Total volumes reached approximately 1.6 million units, representing a 17% YoY decline. The Passenger Vehicle (PV) segment fell by 20% YoY to 1.4 million units, remaining the primary drag on overall performance, while the Light Commercial Vehicle (LCV) segment posted a moderate 12% YoY increase to 195k units. The seasonally adjusted annualized selling rate (SAAR) in January was 16.5 million units, down 32% from the same period last year. The weaker-than-expected performance was mainly attributable to the high base generated by the pre-Spring Festival sales boom in early 2025, coupled with an earlier Spring Festival holiday that compressed effective selling days in January. The persistent divergence between PVs and LCVs underscored resilient demand for logistics and business operation-related vehicles. China’s Light Vehicle (LV) production reached 2.3 million units in January, a 2.1% YoY decrease. PV output, accounting for 88% of the total, declined by 4.5% YoY to 2.0 million units, reflecting relatively resilient consumer demand and market stability, while in contrast, Commercial Vehicle (CV) production surged by 20.7% YoY to 279k units. Domestic Chinese OEMs recorded their first output decline in 2026, edging down by 0.9% YoY to 1.6 million units. Meanwhile, joint venture (JV) OEMs remained under pressure, with volumes falling by 4.5% YoY. A key explanation for the far milder production decline relative to sales—with a 17% YoY drop in total sales compared to a 2.1% YoY drop in production—was strong support from auto exports, which effectively offset weak domestic demand and prevented a deeper production contraction. During the month, China’s LV exports reached 639k units, posting a robust expansion of 45.4% YoY despite suffering a 9.2% month-on-month (MoM) decrease. Growth was led mainly by PVs, with overseas shipments rising by 49.0% YoY to 583k units. CV exports also recorded steady expansion, increasing by 16.9% YoY to 56k units. This strong export performance directly supported manufacturers in maintaining relatively stable production volumes. On December 30, 2025, eight ministries—including the Ministry of Commerce—officially unveiled the 2026 Auto Trade-in Subsidy Implementation Rules. Compared with the 2025 policy, the new regulation is more targeted and refined, shifting from broad-based stimulus to precise and restrained support. Major changes affecting market forecasts include the shift from fixed-amount subsidies to a purchase-price percentage-based mechanism, together with differentiated subsidy rates designed to encourage targeted consumer behavior. This structural shift links subsidy values more closely to transaction prices, introducing greater uncertainty in assessing the overall stimulus impact. In addition, the intensive policy stimulus in 2025 had pulled forward a portion of consumer demand. Against this backdrop, we regard Q1 2026 as a transitional period for policy adaptation and a gradual recovery phase following front-loaded consumption. In January, New Energy Vehicle (NEV) production reached 958k units, representing a 1% YoY decrease and a sharp 39% MoM decline. Beyond seasonal factors, this slowdown was partly driven by consumers delaying purchases in anticipation of the newly released trade-in policy. In terms of market structure, Battery Electric Vehicles (BEVs) recorded a slight decline in market share, while Plug-in Hybrid Electric Vehicles (PHEVs) and Extended Range Electric Vehicles (EREVs) gained momentum. During the Spring Festival holiday, some consumers prioritized long-distance travel practicality and shifted toward hybrid models due to range concerns over pure Electric Vehicles (EVs). Furthermore, the accelerated expansion of charging infrastructure has improved the charging efficiency of hybrid vehicles, further supporting their growing popularity. In 2026, China’s auto market is expected to enter a critical phase, shifting from “scale competition” to “capability competition.” From a policy perspective, adjustments to the purchase tax for NEVs, the updated trade-in subsidy program, and a stricter dual-credit policy will directly affect consumers’ vehicle purchase costs and automakers’ strategic direction. Policy guidance is shifting from broad-based stimulus to more targeted support. Over the long term, the new policies appear more sustainable. First, subsidies are linked to new-vehicle prices, helping to prevent the previous practice of “profiteering” through low-priced models and ensuring fiscal resources are directed more precisely toward upgrading consumer demand. Second, earlier clarification of policy details should help stabilize consumer expectations and reduce irrational, last-minute purchasing spikes driven by prior years’ policy-expiration deadlines. Based on current conditions, we expect the domestic market in 2026 to post slight growth or remain flat, broadly in line with 2025, while exports should sustain double-digit growth. NEVs, overseas markets, and lower-tier markets will remain the core growth drivers, and industry transformation may accelerate further, intensifying consolidation and speeding up the “survival-of-the-fittest” cycle. "China’s light vehicle market expected to be flat in 2026" was originally created and published by Just Auto, a GlobalData owned brand. The information on this site has been included in good faith for general informational purposes only. It is not intended to amount to advice on which you should rely, and we give no representation, warranty or guarantee, whether express or implied as to its accuracy or completeness. You must obtain professional or specialist advice before taking, or refraining from, any action on the basis of the content on our site.