yahoo Press

Semiconductor Opportunity Is Here

Images

1 / 6

2 / 6

3 / 6

4 / 6

5 / 6

6 / 6

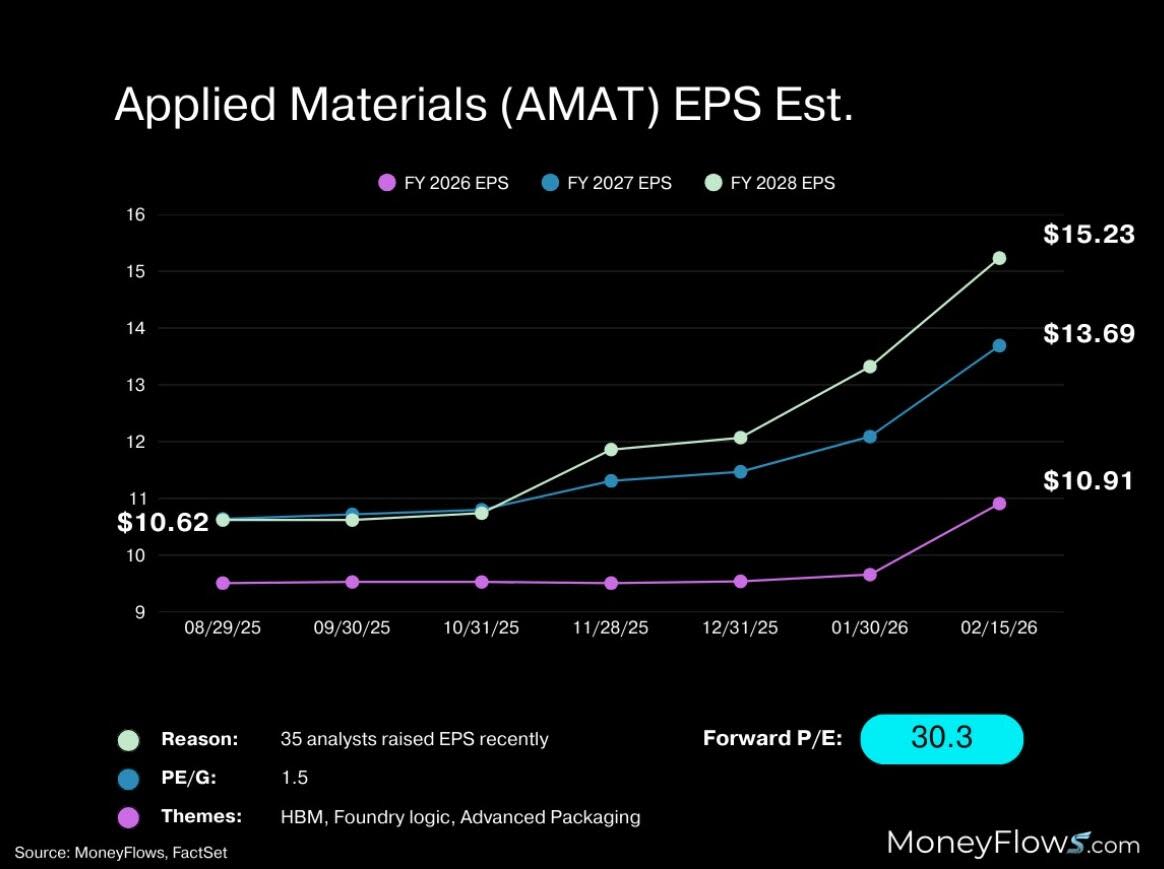

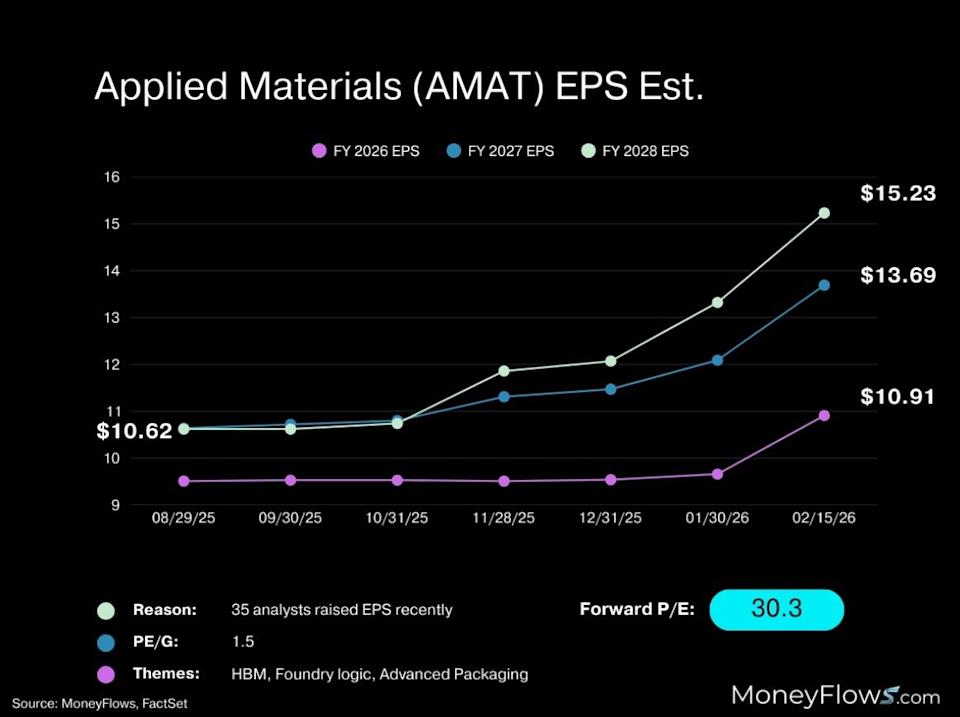

Of course, that means the AI trade. You may have heard that it’s dead. I’m here to tell you it’s not. Last year, pretty much anything associated with AI (or maybe even mentioning the technology) went up in value. This year that’s not the case. Some technology stocks have suffered this year. But not all AI-related firms are lumped in with that group. In fact, I think many companies directly in the AI mix have a lot more room to run. It’s clear when you examine the fundamentals. Plus, many large semiconductor firms are trading below analyst price targets. That all means semiconductor opportunity is here. Applied Materials, Inc. (AMAT) is a nearly $300 billion market cap chip manufacturer. Its shares have been on a huge run, gaining 39% so far this year. The company’s first-quarter fiscal 2026 earnings report was solid, with $7 billion in revenue and non-GAAP per-share earnings of $2.38. More importantly, the company’s quarterly revenue guidance called for $7.65 billion (9.1% above consensus), with EPS guidance of up to $2.84 (15.8% above expectations). The fundamental picture is strong: 1-year EPS estimate (+26.3%) 3-year EPS growth rate (+5.2%) Profit margin (+24.7%) Source: FactSet When earnings are projected to soar, the stock has nowhere to go but up: So, it’s not surprising to see so many institutional inflows: Smart money is often first to trends. Another semiconductor name poised for more growth is foundry firm Taiwan Semiconductor Manufacturing Co., Ltd. (TSM), or TSMC. The massive $1.5 trillion market cap company is a primary player in the AI race. The company’s fourth-quarter fiscal 2025 earnings report showed $33.7 billion in revenue and a 46.4% rise in EPS. Guidance calls for up to $35.8 billion in first-quarter 2026 revenue. TSM’s fundamentals are excellent: 3-year sales growth rate (+19%) 3-year EPS growth rate (+21.9%) Profit margin (+45.1%) Source: FactSet And that’s why we see almost a full year’s worth of Big Money inflows: TSM has a track record of profitable performance and seems to be on course for a similarly positive future path. Lastly, KLA Corporation (KLAC) is another semiconductor standout. The $200 billion chip equipment maker has gained 99.7% in a year delivering needed packaging as AI demands accelerate. Earnings-wise, its second-quarter fiscal 2026 report showed full-year revenue of over $12.7 billion (a 17% year-over-year gain) and a 29% rise in EPS. The fundamental picture is clear: 1-year sales growth rate (+24%) 3-year EPS growth rate (+14.6%) Profit margin (+33.4%) Source: FactSet And the company is positioning for more growth, based on its capital expenditures: Institutions agree on more growth, based on the flurry of inflows: KLA could see its shares soar even more down the road. With markets flat overall, it’s a stock picker’s year so far. And MoneyFlows data is spotting the winners. The news isn’t catching these inflows. You need to dig deeper to see Big Money market movers in action. If you are a Registered Investment Advisor (RIA) or a serious investor, take your investing to the next level and follow our free weekly MoneyFlows insights. Disclosure: the author holds no positions in AMAT, TSM, or KLAC at the time of publication. This article was originally posted on FX Empire Further Strength for the Australian Dollar After Higher Inflation Watch Monster Beverage Soar on Institutional Inflows Watch as Big Money Boosts Analog Devices Walmart Earnings Preview: Can WMT Reach a New All-Time High? (Part One) See Tidewater Rise as Big Money Buys See How Institutions Push Vita Coco Shares Higher