yahoo Press

Opendoor Just Broke Above Its 20-Day Moving Average. Should You Buy OPEN Stock Here?

Images

1 / 7

2 / 7

3 / 7

4 / 7

5 / 7

6 / 7

7 / 7

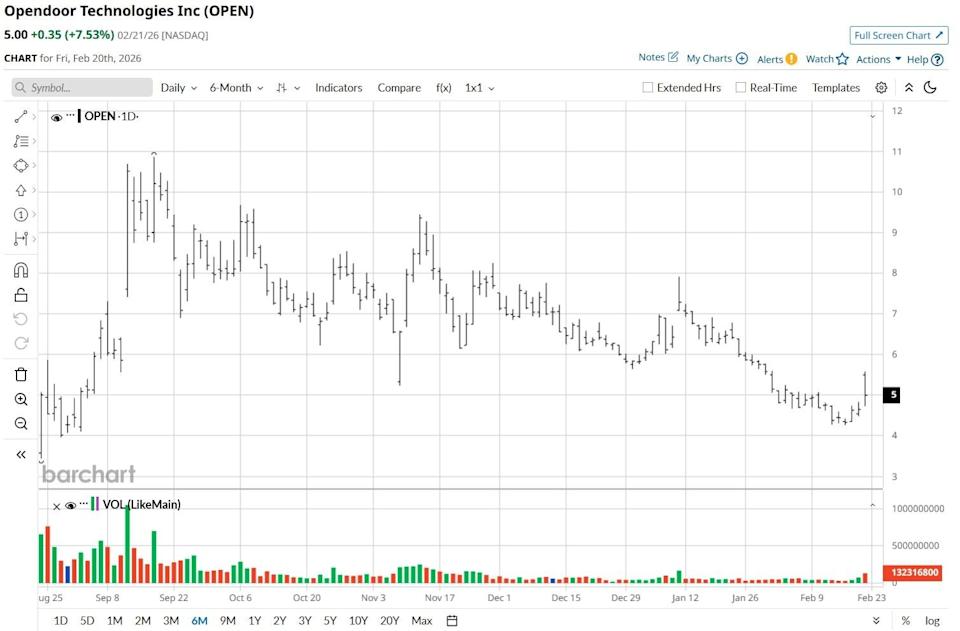

Opendoor Technologies (OPEN) shares ended roughly 10% higher on Feb. 20 after the iBuyer said a 46% sequential increase in home acquisition volume helped it beat Street estimates in its Q4. This post-earnings surge helped OPEN breach its 20-day moving average (MA), indicating upward momentum may sustain in the near term. If Palantir is Near a Bottom, What's the Best Play in PLTR Stock? NVDA Earnings, Tariffs and Other Key Things to Watch this Week Adobe (ADBE) Stock Has Been Beaten Up But the Smart Money Remains Resilient Tired of missing midday reversals? The FREE Barchart Brief newsletter keeps you in the know. Sign up now! Still, a deeper dive reveals significant challenges that warrant caution in playing Opendoor stock that’s now hovering around $5. Opendoor did come in ahead of revenue estimates for its fiscal Q4 but the number – nonetheless – was down some 32% year-over-year, signaling continued weakness in the underlying housing market U.S. pending home sales hit an all-time low in January, and home price growth has slowed to 0.9% only, creating a precarious environment for the iBuying business model. Moreover, while OPEN stock pushed past its 20-day MA on Friday, it remains decisively below its longer-term averages (50-day, 100-day), reinforcing that the broader downtrend remains intact. Opendoor shares remain unattractive also because the management’s commitment to profitability by year-end faces significant macroeconomic headwinds. With $2 billion in net debt and gross margins set at 8.2% only, OPEN has limited financial cushion should rising supply meet weakening home prices. Opendoor’s reliance on rapid inventory turnover becomes increasingly risky when buyer demand remains subdued, with 55% of homeowners locked into sub-4% mortgages unlikely to transact at current rates. Adding to the risks, OPEN remains a penny stock, which often means heightened volatility, limited institutional support, and weaker investor confidence. Chasing the momentum in such names often trap late investors in a downward spiral once the hype cools. Wall Street firms also believe the recent rally in OPEN shares has gone a bit too far and, therefore, runs the risk of a sharp reversal over the next few weeks. The consensus rating on Opendoor Technologies sits at “Hold” only, with the mean target of about $3.48 indicating potential downside roughly 30% from here. This article was created with the support of automated content tools from our partners at Sigma.AI. Together, our financial data and AI solutions help us to deliver more informed market headline analysis to readers faster than ever. On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. This article was originally published on Barchart.com